Urbanization

How the Expansion of Megacities Will Boost Metal Markets

How the Expansion of Megacities Will Boost Metal Markets

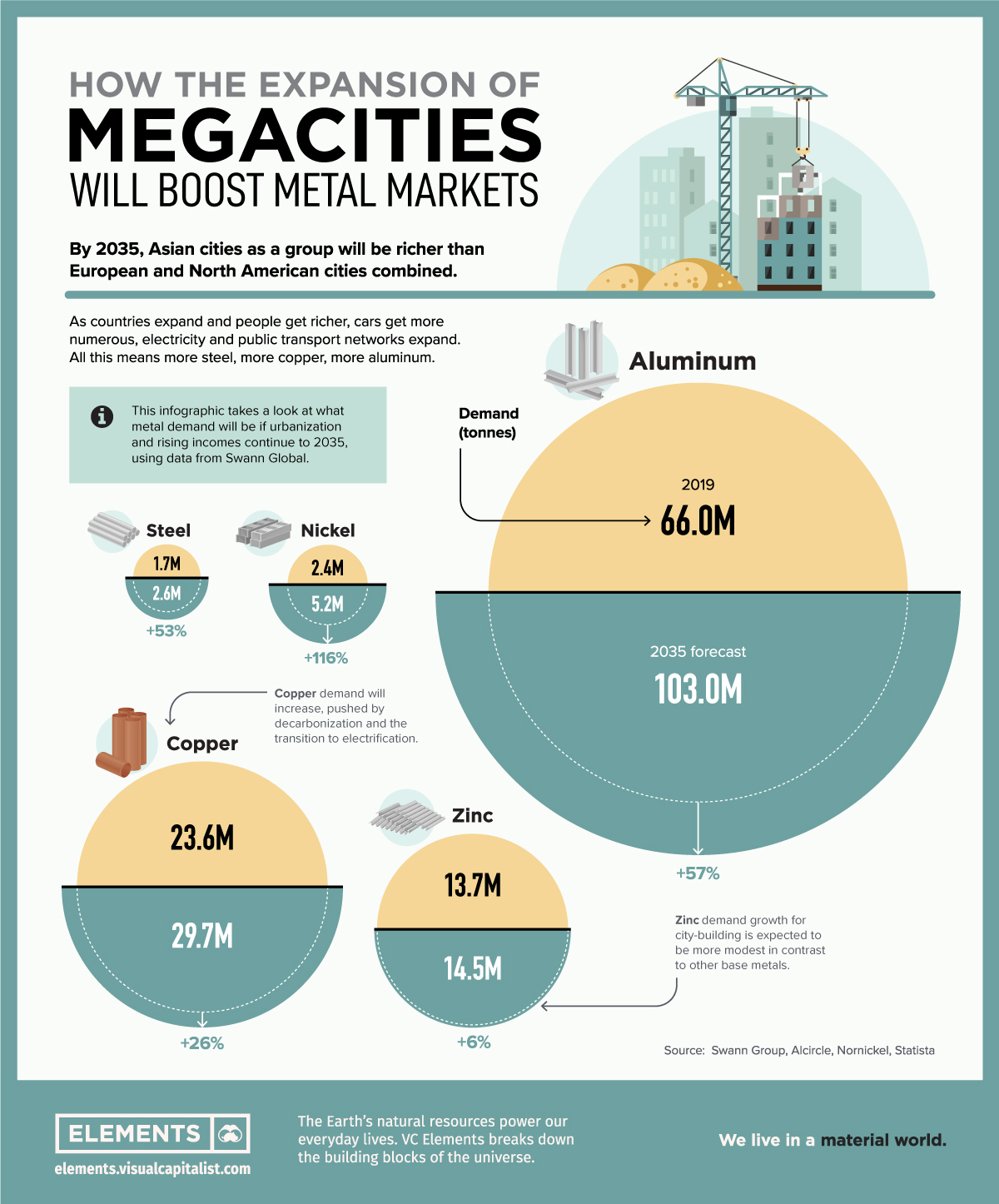

Urbanization drives metal demand, and megacities are leading the drive.

As developing economies grow, millions of people are moving to cities to pursue opportunities compounded by proximity and availability to resources. Many of these people see their economic circumstances improve, and consumption increases as a result.

Cars get more numerous, electricity and public transport networks expand, and consumers buy more electronic products for their homes. All of this means more steel, more copper, more aluminum, and more cement are needed.

The rise of China’s megacities in recent decades embodies this growth of living standards and demand for resources. By 2035, Oxford Economics forecasts that Asian cities as a group will be richer than European and North American cities combined, with six Chinese cities on the list of the 10 richest cities globally: Beijing, Chongqing, Guangzhou, Shanghai, Shenzhen, and Tianjin.

By 2035 these six cities are expected to double their wealth, while global average income per capita is expected to increase by only 37% during the same period.

This infographic, based on research from Swann, takes a look at how the growth of megacities will drive metal demand well into the future.

Megacities Metal Megatrend: Growth in Demand to 2035

The Swann Index measures the intensity of use of each metal by looking at global consumption in tonnes between 2014 and 2019, dividing by GDP per capita, and then forecasting demand up until 2035. Here are some key materials and how they are expected to fare:

| Metal | Demand (tonnes, 2019) | Demand (tonnes, 2035) | Change (2019–2035) |

|---|---|---|---|

| Nickel | 2.4 | 5.2 | 116% |

| Steel | 1.7 | 2.6 | 50% |

| Aluminum | 66.0 | 103.6 | 57% |

| Copper | 23.6 | 29.7 | 26% |

| Zinc | 13.7 | 14.5 | 6% |

Nickel demand is forecast to increase by 116%, from 2.4 million tonnes in 2019 to 5.2 million tonnes in 2035. The drive is fueled by consumer goods, batteries, and high-value new applications, such as super alloys and stainless steel.

Aluminum and steel are also expected to see significant growth of 57% and 50%, respectively. Aluminum’s growth will be particularly noticeable due to the market size, with an expected demand of 103.6 million tonnes in 2035.

Copper’s demand growth will largely be pushed by decarbonization and the transition to electrification and automated technology. The metal is expected to see demand increase by 26% to 29.7 million tonnes in 2035.

In comparison, zinc is likely to underperform other base metals, with an estimated increase of only 6%. This modest growth reflects strong competition from aluminum in some end-use markets such as diecast alloys.

Future Megacities on the African Horizon

Though megacity demand for metals is being driven largely by Asian growth in 2020, the focus will likely shift in the coming decades.

Projections of future population growth and the world’s biggest cities all point to Africa as the next leader in growth, and subsequently, demand. Estimates show that 17 of the 20 fastest growing cities from 2020 to 2025 are located in Africa.

By 2100, the world’s three largest cities with populations greater than 70 million are projected to be in Africa, with Nigeria’s Lagos leading the way. In fact, of the world’s 20 largest projected megacities, 13 will be in Africa and zero will be located in China.

For now, Asian and primarily Chinese cities are leading demand for urbanization materials and already putting a strain on some metals. Even though the future megacity landscape might change, the expected continued increase in economic growth and incomes will continue to drive metal demand.

Urbanization

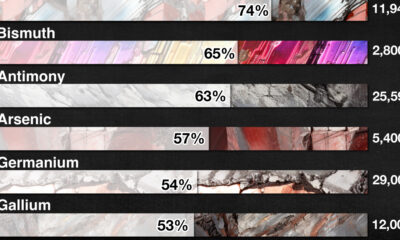

Ranked: The 20 Most Air-Polluted Cities on Earth

Using 2022 average PM2.5 concentrations, we rank the most polluted cities in the world.

Ranked: The 20 Most Air-Polluted Cities on Earth

According to the World Health Organization (WHO), almost the entire global population (99%) breathes air that exceeds WHO air quality limits.

In the above map, we use 2022 average PM2.5 concentrations from IQAir’s World Air Quality Report to visualize the most air-polluted major cities in the world.

World’s Air Pollution Hot Spots

As one of the standard air quality indicators used by the WHO, the PM2.5 concentration refers to the quantity of fine particulate matter with a diameter of 2.5 micrometers or less in a given volume of air.

Fine particulate matter that is this small can penetrate the lungs when inhaled and enter the bloodstream, affecting all major organs.

Based on annual average PM2.5 concentrations (μg/m³) in 2022, here are the most polluted cities in the world.

| Rank | City | 2022 average PM2.5 concentration (μg/m³) |

|---|---|---|

| 1 | 🇵🇰 Lahore, Pakistan | 97.4 |

| 2 | 🇨🇳 Hotan, China | 94.3 |

| 3 | 🇮🇳 Bhiwadi, India | 92.7 |

| 4 | 🇮🇳 Delhi, India | 92.6 |

| 5 | 🇵🇰 Peshawar, Pakistan | 91.8 |

| 6 | 🇮🇳 Darbhanga, India | 90.3 |

| 7 | 🇮🇳 Asopur, India | 90.2 |

| 8 | 🇹🇩 N'Djamena, Chad | 89.7 |

| 9 | 🇮🇳 New Delhi, India | 89.1 |

| 10 | 🇮🇳 Patna, India | 88.9 |

| 11 | 🇮🇳 Ghaziabad, India | 88.6 |

| 12 | 🇮🇳 Dharuhera, India | 87.8 |

| 13 | 🇮🇶 Baghdad, Iraq | 86.7 |

| 14 | 🇮🇳 Chapra, India | 85.9 |

| 15 | 🇮🇳 Muzaffarnagar, India | 85.5 |

| 16 | 🇵🇰 Faisalabad, Pakistan | 84.5 |

| 17 | 🇮🇳 Greater Noida, India | 83.2 |

| 18 | 🇮🇳 Bahadurgarh, India | 82.2 |

| 19 | 🇮🇳 Faridabad, India | 79.7 |

| 20 | 🇮🇳 Muzaffarpur, India | 79.2 |

With numbers these high, the concentration of some or all of the following pollutants are at dangerous levels in these cities:

- Ground-level ozone

- Particulate matter

- Carbon monoxide

- Sulfur dioxide

- Nitrogen dioxide

At the top of the list, Lahore in Pakistan has a combination of high vehicle and industrial emissions, as well as smoke from brick kilns, crop residue, general waste burning, and dust from construction sites.

Air pollution levels can also be impacted by practices such as large-scale tree removal in order to build new roads and buildings.

As a result of its growing population and rapidly expanding industrial sector, India has 14 cities on the list, outpacing China, formerly considered the world’s number one air pollution source.

The only African country on the list, Chad, experienced severe dust storms in 2022 that resulted in an 18% increase in PM2.5 concentration in 2022 compared to the previous year.

The Cost of Poor Air Quality

Poor air quality is one of the leading causes of early deaths worldwide, just behind high blood pressure, tobacco use, and poor diet.

According to a 2020 study by the Health Effects Institute, 6.67 million people died as a result of air pollution in 2019.

In addition to the millions of premature deaths each year, the global cost of health damages associated with air pollution currently sits at $8.1 trillion.

Urbanization

Visualizing the World’s Largest Steel-Producing Countries

China has dominated global steel production the past few decades, but how did the country get here, and is its production growth over?

The Largest Steel-Producing Countries: Visualized

Steel is a critical component of modern industry and economy, essential for the construction of buildings, automobiles, and many other appliances and infrastructure used in our daily lives.

This graphic uses data from the World Steel Association to visualize the world’s top steel-producing countries, and highlights China’s ascent to the top, as it now makes up more than half of the world’s steel production.

The State of Global Steel Production

Global steel production in 2022 reached 1,878 million tonnes, barely surpassing the pre-pandemic production of 1,875 million tonnes in 2019.

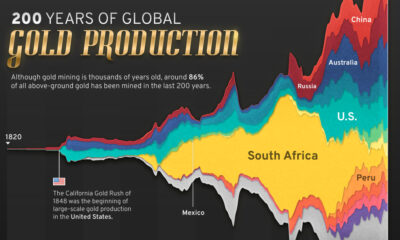

| Country | 2022 Production (in million tonnes) | Annual Production Change | Global Share |

|---|---|---|---|

| 🇨🇳 China | 1013.0 | -2.0% | 53.9% |

| 🇮🇳 India | 124.8 | 5.3% | 6.6% |

| 🇯🇵 Japan | 89.2 | -7.9% | 4.8% |

| 🇺🇸 United States | 80.5 | -6.5% | 4.3% |

| 🇷🇺 Russia | 71.5 | -5.8% | 3.8% |

| 🇰🇷 South Korea | 65.9 | -6.9% | 3.5% |

| 🇩🇪 Germany | 36.8 | -8.8% | 2.0% |

| 🇹🇷 Türkiye | 35.1 | -15.0% | 1.9% |

| 🇧🇷 Brazil | 34.0 | -6.5% | 1.8% |

| 🇮🇷 Iran | 30.6 | 6.8% | 1.6% |

| 🇮🇹 Italy | 21.6 | -13.0% | 1.1% |

| 🇹🇼 Taiwan | 20.7 | -12.1% | 1.1% |

| 🇻🇳 Vietnam | 20.0 | -15.0% | 1.1% |

| 🇲🇽 Mexico | 18.2 | -1.9% | 1.0% |

| 🇮🇩 Indonesia | 15.6 | 8.3% | 0.8% |

| Rest of World | 201.0 | -11.2% | 10.7% |

| World Total | 1878.5 | -3.9% | 100.0% |

2022’s steel production marked a significant reduction compared to the post-pandemic rebound of 1,960 million tonnes in 2021, with a year-over-year decline of 4.2%–the largest drop since 2009, and prior to that, 1991.

This decline was spread across many of the world’s top steel producers, with only three of the top fifteen countries, India, Iran, and Indonesia, increasing their yearly production. Most of the other top steel-producing countries saw annual production declines of more than 5%, with Turkey, Italy, Taiwan, and Vietnam’s production all declining by double digits.

Even the world’s top steel-producing nation, China, experienced a modest 2% decline, which due to the country’s large production amounted to a decline of 19.8 million tonnes, more than many other nations produce in a year.

Despite India, the world’s second-largest steel producer, increasing its production by 5.3%, the country’s output still amounts to just over one-tenth of the steel produced by China.

China’s Meteoric Rise in Steel Production

Although China dominates the world’s steel production with more than a 54% share today, this hasn’t always been the case.

In 1967, the World Steel Association’s first recorded year of steel production figures, China only produced an estimated 14 million tonnes, making up barely 3% of global output. At that time, the U.S. and the USSR were competing as the world’s top steel producers at 115 and 102 million tonnes respectively, followed by Japan at 62 million tonnes.

Almost three decades later in 1996, China had successively overtaken Russia, the U.S., and Japan to become the top steel-producing nation with 101 million tonnes of steel produced that year.

The early 2000s marked a period of rapid growth for China, with consistent double-digit percentage increases in steel production each year.

The Recent Decline in China’s Steel Production

Since the early 2000s, China’s average annual growth in steel production has slowed to 3.4% over the last decade (2013-2022), a considerable decline compared to the previous decade’s (2003-2012) 15.2% average annual growth rate.

The past couple of years have seen China’s steel production decline, with 2021 and 2022 marking the first time the country’s production fell for two consecutive years in a row.

While it’s unlikely China will relinquish its position as the top steel-producing nation anytime soon, it remains to be seen whether this recent decline marks the beginning of a new trend or just a brief deviation from the country’s consistent production growth.

-

Electrification3 years ago

Electrification3 years agoRanked: The Top 10 EV Battery Manufacturers

-

Electrification2 years ago

Electrification2 years agoThe Key Minerals in an EV Battery

-

Real Assets3 years ago

Real Assets3 years agoThe World’s Top 10 Gold Mining Companies

-

Misc3 years ago

Misc3 years agoAll the Metals We Mined in One Visualization

-

Electrification3 years ago

Electrification3 years agoThe Biggest Mining Companies in the World in 2021

-

Energy Shift2 years ago

Energy Shift2 years agoWhat Are the Five Major Types of Renewable Energy?

-

Electrification2 years ago

Electrification2 years agoThe World’s Largest Nickel Mining Companies

-

Electrification2 years ago

Electrification2 years agoMapped: Solar Power by Country in 2021